Table of Contents

Introduction

Business insurance is another trick in the sleeve of the entrepreneur.Owners need professional insurance. Generally, states are granting business owners a requirement of having a general liability insurance by law. However, there’s no way to enter the office of the insurance company and ask them, “Will you please provide me with commercial insurance?” Even more surprisingly, there is almost as many business insurance types as their are business types, and nobody may be able to suggest a good fit.

What is Business Insurance?

Business insurance calls all those insurance types, the policy of which covers the financial damages taken by your business. Dependent on such policy, commercial insurance entails offering plenty of coverage such as for property damage, public liability, medical expenses, and more which are all aimed to cover medical risks.

Let’s examine what types of insurance policies maximum small businesses need, what risks these policies protect them against, and why enterprises buy them. Hopefully, this will help business owners looking to manage their potential risks with insurance make the right decisions and get suitable types of business insurance.

What are the Types of Business Insurance?

Professional insurance policies may do organized into packages based on your industry, such as insurance for cleaning companies or insurance for independent contractors. Typically, these packages include a combination of the following types of coverage.

Why Timely Business Insurance Renewal Matters

Business insurance renewal keeps your operations safe from lawsuits, fires, floods, or cyber attacks—lapses cost fines or bankruptcy. For Hyderabad SMEs, first-party (comprehensive) covers own damage + liability; renew 60 days early via HDFC ERGO or Bajaj.

Types of Business Insurance

Pick coverage matching your risks—1-year terms standard.

| Type | Duration | Monthly Premium (Small Biz) | Benefits | Top Providers |

|---|---|---|---|---|

| General Liability | 1 year | ₹500-₹2k | Claims, legal fees | HDFC ERGO, ICICI Lombard |

| Property | 1 year | ₹300-₹1.5k | Fire/theft protection | Tata AIG, New India |

| Workers Comp | 1 year | ₹400-₹1.8k | Employee injuries | Reliance, SBI General |

| Cyber | 1 year | ₹700-₹4k | Hacks, data recovery | ICICI, Digit |

| BOP | 1 year | ₹800-₹5k | All-in-one bundle | HDFC ERGO |

Top Providers in India 2026

Ranked by CSR, networks for fast claims.

| Rank | Provider | CSR % | Garages | Best For |

|---|---|---|---|---|

| 1 | HDFC ERGO | 99 | 8,200+ | Digital SMEs |

| 2 | Bajaj Allianz | 98.5 | 4,000+ | Manufacturing |

| 3 | ICICI Lombard | 96.75 | 5,900+ | IT firms |

| 4 | Tata AIG | 76 | 7,500+ | Logistics |

Payment Plans: Monthly vs Annual

Annual saves cash; monthly eases flow.

| Aspect | Annual | Monthly |

|---|---|---|

| Cost | ₹10k → ₹8.5k (10% off) | ₹10k → ₹11.5k (+15%) |

| Cash Flow | Lump sum hit | Spread out |

| Best For | Stable revenue | Startups |

How to Choose the Right Policy

- List risks (e.g., Hyderabad floods).

- Match types (BOP for small biz).

- Compare CSR >95%, limits ₹1cr+.

| Factor | Check For |

|---|---|

| CSR | >95% |

| Premium | 1-3% turnover |

| Add-ons | Local disasters |

Questions for Brokers

Vet via Policybazaar or Mitigata.

| Category | Key Questions |

|---|---|

| Experience | Years with SMEs? References? |

| Coverage | Risks covered? Exclusions? |

| Claims | Turnaround time? Assist? |

| Costs | Fees? Discounts? |

Tech Tools Simplify Management

Apps handle everything.

| Feature | Advantage |

|---|---|

| Policy View | Edit/pay online |

| Claims | Track status |

| Quotes | Compare fast |

| Docs | Instant access |

Common Renewal Myths

| Myth | Fact |

|---|---|

| Auto-renew OK | Review needs yearly |

| No drive, no need | Liability still applies |

| Minor changes skip notice | Update vehicle/driver info |

Timely renewal via annual payments maximizes savings—contact HDFC ERGO today for Hyderabad flood cover.

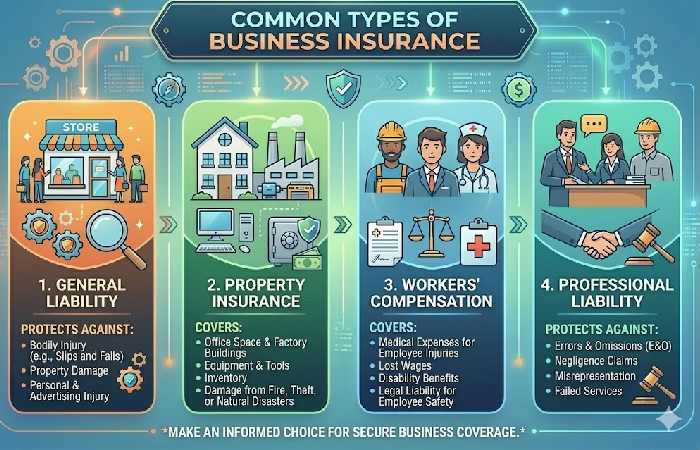

General Liability

General liability insurance is tailored to defend against claims that may potentially come from the business’s contents and procedures. Illustrating that, one of your visitors for example, injured themselves at your workplace or damaged somebody else’s property, customers’ safety is paramount.

For example, suppose you own a retail store. A customer errors and falls in your lobby and breaks his arm. They are seeking compensation for mental trauma from you, and the judge orders to pay them with $100,000 of money to suffer damages. If you have general liability insurance, your insurer will cover the damages and cure of your legal costs.

Compensation Business Insurance

Employer’s liability for work-related injuries or sicknesses, known in the business jargon as “workers’ compensations”, are included in the business coverage. Offers coverage for medical costs and gone wages if a worker is injured while working. Sometimes, it also covers the cost of your legal protection if the employee sues you. In addition. Sometimes disability insurance is included with workers’ compensation.

For example, let’s say you own a minor clothing line. If one of your workers is injured while tapestrying. Your workers’ compensation insurance will protect the cost of their medical treatment and lost wages.

Commercial Property

This type of defends your assets against damage or theft. For example, if your office does damage by fire or your computer apparatus is stolen. This insurance will reimburse you for repairs or replacement and lost income. Any physical assets needs commercial property insurance.

For example, suppose you own an accountancy firm, and your office does rob. Steals steal your computer, printer, and office furniture. If you have profitable property insurance, your insurer will repay you for the cost of repairs or replacement and any income you lost. At the same time, your crew was inept at working, payable to a lack of equipment.

Professional Liability Business Insurance

It is also known by the names ‘mistake’ or ‘omission’ liability insurance and serves to insure the business against the cost of damage or injury claims arising from the professional conduct of the business. Let us say you are providing a service to your clients and they account that you failed to do your job correctly and it has caused a loss, your insurance covers the cost of your defense as well as compensate any damages.

For example, suppose you are an architect. You designed a house for a client. And they said the roof leaked through the first storm because your design was terrible. If you sue, your qualified liability insurance will cover your legal outlays and any damages awarded.

Conclusion

By understanding the types of business insurance available, you can ensure that your adequately covers an accident or disaster. Of course, no company is immune to risk, but you can protect your with the right policies.